Once again, the March budget season has arrived, and Rep. Paul Ryan (R-WI) has engineered another draconian fiscal vision for the House Republicans. The plan would radically remake Medicare, decimate Medicaid, grant a huge tax cut to the wealthy, and slash support for the poor, investments, and civic infrastructure.

Once again, the March budget season has arrived, and Rep. Paul Ryan (R-WI) has engineered another draconian fiscal vision for the House Republicans. The plan would radically remake Medicare, decimate Medicaid, grant a huge tax cut to the wealthy, and slash support for the poor, investments, and civic infrastructure.

Ryan and his cohorts justify these plans by insisting that America faces a “debt crisis,” that the deficits we’re currently running are too high, and that we must act immediately to fix these problems. Centrists and other “serious” pundits and lawmakers throughout Washington have bought this argument, if not all the details of Ryan’s specific solution, and they’ve scoffed at President Obama’s insistence that we don’t actually face a looming debt crisis. Here are the reasons Obama’s right, and they’re all wrong:

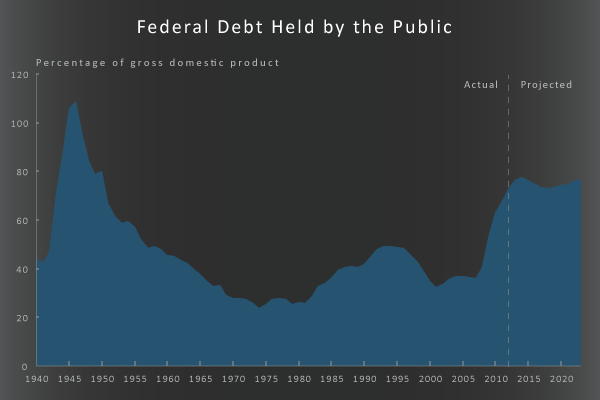

1. We don’t ever have to actually eliminate the debt: The United States ran up a huge debt burden in World War II. More importantly, in raw dollar terms, we never repaid that debt. We simply grew the economy so that the size of the debt fell in comparison. That’s what’s happening in graphs where the debt burden drops in the post-war years. That burden is measured as a ratio of debt-to-GDP, and in ratios the denominator matters as much as the numerator.

{kind=link}

2. The budget doesn’t actually have to balance to reduce it: If we can keep deficits under a certain threshold every year, then economic growth will overtake it, meaning our debt-to-GDP ratio will either stay the same or even drop. For the immediate future, the economic looks set to grow by about 4 percent a year. If we can keep each year’s deficit to 4 percent or less of public debt already held, debt-to-GDP will stabilize. America can, in fact, run deficits in perpetuity.

3. The debt is already as balanced as it needs to be: Federal spending involves a host of programs called “stabilizers” — spending that automatically kicks in when the economy tanks, without any acts on the part of lawmakers, boosting GDP growth and helping Americans who have lost their jobs. These include unemployment insurance, food stamps, welfare, Medicaid, and many others. Tax revenues also naturally fall as unemployment rises.

The Congressional Budget office just released a report that stabilizers will add $422 billion to the deficit in 2013. That leaves $423 billion — out of the estimated $845 billion deficit for the year — that isn’t due to the automatic stabilizers. Publicly held U.S. debt is currently around $11.5 trillion, and $423 is less than 4 percent of that.

Take out the stabilizers, and the deficit is within the window necessary to stabilize the debt. And all we have to do to unwind the stabilizers is get the economy firing on all cylinders again. This holds true for about the next decade, before growth in Social Security, Medicare, and Medicaid finally begin to slowly overtake it. The country still has problems, but it has lots of time to sort them out.

4. The “debt crisis” is not a certainty: Paul Ryan may talk as if it is, but it’s merely a projection — one possible result if the CBO’s guesswork about the future proves accurate. The Center for American Progress recently dove into CBO’s methodology, and found that the projections build in a host of sometimes-dramatic assumptions about Congress’ future spending and taxation choices, as well as other factors that could very well not come to pass.

\ABS\Auto Blog Samurai\data\Obama Care\thinkprogress\LindenLongTermDebt-e1363198339732.png "LindenLongTermDebt")

Beyond trying to predict future Congress’ policy preferences, much of the future debt is based on projections that health care costs will continue growing at their previous trend. But the whole point of health care reform is to alter that trend by altering health care markets. Obamacare may already be doing this. CBO’s projections for Medicare spending over the next decade dropped by $500 billion between 2010 and 2013, simply because health care cost growth unexpectedly slowed.

In fact, if that slowdown becomes the new norm, Medicare spending will stay essentially flat as a share of the economy from here on out. That doesn’t show up in CBO’s long-term projections because their methodology uses cost growth over the last two decades to predict future trends. (See page 60.) It’s literally within the realm of reasonable possibility that the long-term debt problem is already solved — all without lawmakers having to cut a dime.

5. We don’t know how much debt actually causes crisis: Ryan and others often cite a finding that economic growth slows as debt-to-GDP reaches 90 percent. But there’s a big correlation-causation problem with this. Remember the denominator: slowing GDP, regardless of debt, could raise debt-to-GDP just as much as higher debt could. And the countries that fit with the 90 percent threshold prediction also present an apples-to-oranges problem when compared to America. Britain, Japan, and France — advanced democracies like ours, with their own currency — shouldered debt levels far in excess of 90 precent over extended periods of time in the past. No debt crisis arrived.

In conclusion: the “debt crisis” is a mere phantom — only one of many possible futures, and far from a certainty. The interest America is paying on its debt is currently lower than it was in the 1990s, despite a lower debt-to-GDP ratio then. When inflation is factored in, current real interest rates on our debt are negative. Financial markets are willing to pay us to borrow from them.

Meanwhile, every dollar we cut — nay, every dollar we fail to borrow — is a dollar that isn’t going to shore up the safety net, to rebuild the country’s infrastructure, or to support struggling Americans while their livelihoods remain on the line. That we’re passing on this opportunity to repair our country, much less even considering the monstrosity that is the Ryan budget, really is absurd.

0 comments:

Post a Comment